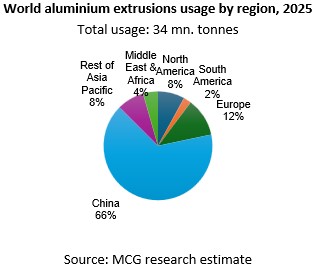

The aluminium extrusions market across the world is growing, driven by demand from construction, automotive and industrial sectors. Growth in renewable energy and the increasing focus on energy efficiency and emissions reduction are also supporting demand. Between 2015 and 2025, global aluminium extrusion demand rose at about 4% per annum, increasing from 23.3 million tonnes to about 34 million tonnes in 2025. China accounted for about 66% of global extrusion usage, followed by Europe, North America and the rest of Asia-Pacific. On the supply side, the industry is focusing on recycled and low-carbon billet production, alongside investments in larger, higher-capacity presses to enable production of more complex and high-strength profiles.

The building and construction sector is the major end user segment of aluminium extrusions, accounting for 57% of demand, supported by growth in emerging economies and increasing use in green buildings and smart infrastructure. In automotive applications, extrusions support lightweighting across key components, with demand expected to rise further with EV adoption, especially for battery housing and structural components. The electrical, electronics and industrial sectors account for 17% of demand, with applications in busbars, enclosures, heat sinks and machinery, supported by growth in solar energy.

The demand for aluminium extrusions across the globe is projected to grow at about 3.6% annually, to reach around 40.5 million tonnes by 2030. The outlook for aluminium extrusions demand needs to be tempered by the recent geopolitical tensions and policy uncertainty around emission targets across countries. In addition, protectionist measures and evolving carbon regulations across regions could influence the market dynamics.